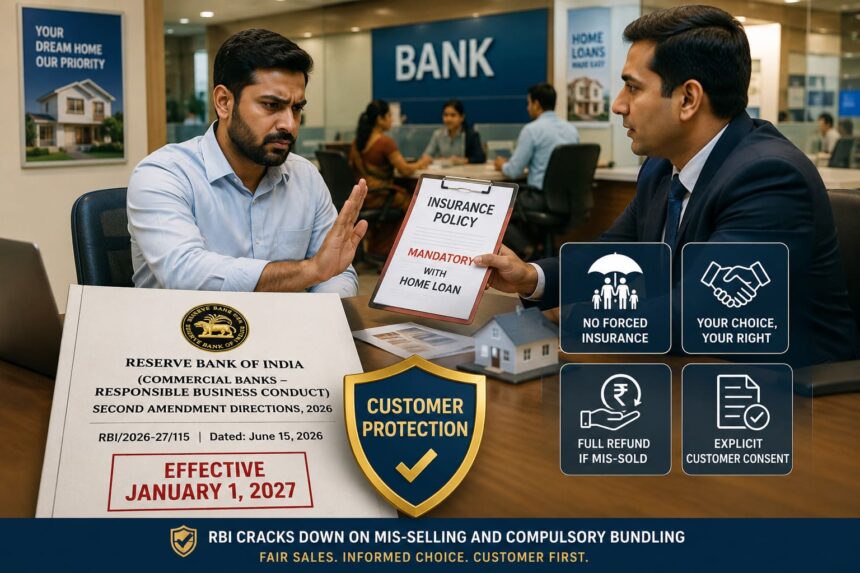

RBI Cracks Down on Mis-Selling and Compulsory Bundling of Financial Products

Buying a home or taking a personal loan often comes with an unexpected requirement from banks – purchasing insurance policies, investment products, or other financial schemes. Many borrowers have complained that these products were pushed on them as a condition for getting their loans approved.

To address these concerns, the Reserve Bank of India (RBI) has issued the Reserve Bank of India (Commercial Banks – Responsible Business Conduct) Second Amendment Directions, 2026 through Circular No. RBI/2026-27/115 (Reference No. DOR.MCS.REC.No.94/01-01-032/2026-27) on June 15, 2026.

The new directions, which will come into force on January 1, 2027, prohibit banks from forcing customers to purchase insurance or other third-party financial products as a condition for availing loans and introduce stricter safeguards against mis-selling, deceptive sales practices and compulsory bundling of financial products.

What Has RBI Changed?

Under the new directions, banks can no longer force customers to purchase:

- Insurance policies

- Unit Linked Insurance Plans and investment products

- Third-party financial products

- Any other add-on financial service as a condition for availing a loan or banking service.

- If insurance is genuinely required as a risk mitigant (for example, a term insurance cover for a home loan), customers can buy it from any insurer of their choice.

If a bank requires insurance as a risk mitigation measure, customers will be free to purchase the policy from any insurer of their choice.

Explicit Customer Consent Now Mandatory

Banks will now be required to obtain the customer’s clear and informed consent before selling any financial product.

The RBI has specifically prohibited:

- Hidden terms and conditions

- Pre-ticked consent boxes

- Assumed customer consent

- Misleading sales practices.

Banks will also need to maintain proper records of the customer’s consent.

Banks Cannot Use Loan Amount to Buy Insurance Without Permission

In several cases, borrowers discovered that a portion of their loan amount had been used to purchase insurance products without their knowledge.

The new rules prohibit banks from using the sanctioned loan amount to purchase insurance or investment products unless the borrower has explicitly agreed to such a transaction.

Mandatory Customer Verification After Every Sale

Banks must now contact customers within 30 days of selling a financial product to confirm:

- Whether the customer understood the product.

- Whether the customer was informed about the risks.

- Whether the purchase was made voluntarily.

This additional verification mechanism is expected to significantly reduce instances of mis-selling.

Full Refund if Mis-Selling is Established

The RBI has also introduced a strong compensation mechanism.

If a customer proves that a financial product was mis-sold:

- The entire amount paid must be refunded.

- The sale can be cancelled.

- Additional compensation may also be payable if the customer suffered losses.

RBI Bans ‘Dark Patterns’

The new directions also target deceptive digital practices commonly referred to as “dark patterns.”

Banks and their agents can no longer use:

- Misleading buttons

- Confusing interfaces

- Hidden consent mechanisms

- Difficult opt-out procedures

- Digital tricks designed to pressure customers into purchasing products.

Banks will be required to periodically review their websites and applications to ensure compliance.

Tighter Rules for Bank Agents and Marketing Personnel

The RBI has imposed stricter oversight on:

- Direct Selling Agents (DSAs)

- Direct Marketing Agents (DMAs)

- Third-party sales personnel.

Banks must establish proper training systems, audits, monitoring mechanisms and accountability standards for their agents.

Customers Can Easily Opt Out of Marketing Messages

Customers will also have a simpler mechanism to:

- Withdraw consent.

- Stop promotional communications.

- Opt out of marketing messages and product offers.

Why These Rules Matter for Homebuyers

Homebuyers are among the biggest beneficiaries of the new framework. Many borrowers have long complained that banks insisted on purchasing expensive insurance products while sanctioning home loans.

From January 1, 2027:

✔ Home loan borrowers cannot be compelled to buy insurance from a bank’s preferred insurer.

✔ Banks cannot automatically add insurance premiums to the loan amount.

✔ Customers will have greater freedom to choose financial products that suit their needs.

✔ Mis-selling complaints will have stronger legal backing.

What Should Borrowers Do?

Whenever you apply for a home loan or any other banking product:

- Carefully review all documents.

- Ask whether any insurance product is optional.

- Avoid signing blank forms.

- Preserve copies of all declarations and consent forms.

- Immediately raise a complaint if you believe a product was sold without your informed consent.

The RBI’s new framework marks one of the biggest customer protection reforms in recent years and is expected to fundamentally change the way banks sell financial products in India.