The transformation of India’s residential real estate market over the past two years highlights a major shift in urban housing dynamics. The sector has successfully moved away from the volatile, speculative spikes of the immediate post-pandemic boom, anchoring itself in long-term, structural growth driven by genuine end-users.

By analyzing the data from the 2025 normalization phase alongside the performance numbers from Q1 and Q2 2026, we get a clear picture of what to expect as the market moves into Q3 2026.

The Reference Point: 2025 Establishes Capital Discipline

The core foundation of the current market was built throughout 2025—a year defined by deliberate developer restraint and stabilizing demand. Rather than flooding major micro-markets with unabsorbable inventory, builders closely aligned new launches with actual buyer intake. This structural equilibrium was highly localized.

Across the top eight cities:

- quarterly new supply held steady (ranging between 84,000 and 93,000 units), while

- sales velocity remained uniform, averaging roughly 95,000 to 98,000 units sold per quarter.

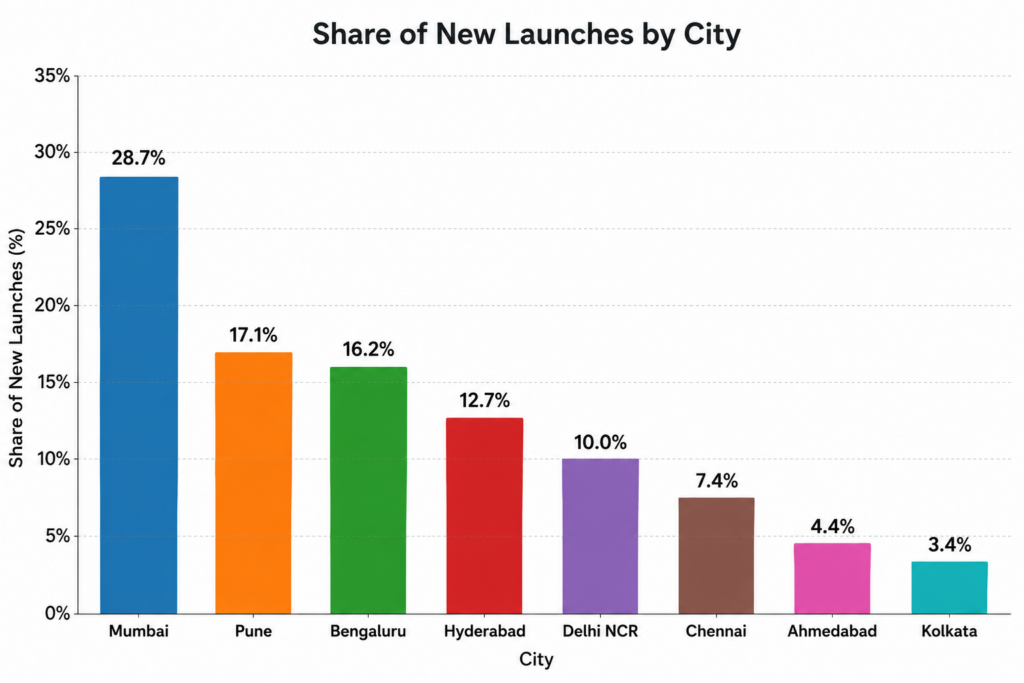

A staggering 74.7% of all new housing launches were concentrated within just four economic powerhouses:

- The Mumbai Metropolitan Region (MMR),

- Pune,

- Bengaluru, and

- Hyderabad.

Speculative flippers cleanly exited the space, leaving behind highly discerning, quality end-users who prioritized premium features, lifestyle upgrades, and Grade-A developer execution over cheap, sub-standard square footage.

The Geographic Playbook: Where India’s Housing is Concentrated

Developer focus in 2025 narrowed down heavily onto micro-markets backed by infrastructural milestones and tech-driven employment.

Share of New Residential Launches by City (2025)

H1 2026 Retrospective: The Premiumization Push

Building directly on top of 2025’s stable baseline, the first half of 2026 pushed the Indian residential market into overdrive—accelerating heavily toward luxury and premiumization. Properties priced above ₹1.5 Crore took center stage, rapidly becoming the primary engine of market growth.

City-by-City Pricing Breakdowns (H1 2026)

- Mumbai (MMR)

- Q1 2026 Average Price: ₹17,600 per sq ft

- Q2 2026 Average Price: ₹17,780 per sq ft

- Market Dynamics: Maintained absolute market dominance. Driven by massive infrastructure works, urban redevelopment, and luxury integrated townships, demand remained robust despite premium pricing tags .

- Delhi-NCR

- Q1 2026 Average Price: ₹9,534 per sq ft

- Q2 2026 Average Price: ₹9,810 per sq ft

- Market Dynamics: The premium and luxury segment priced between ₹2 Crore and ₹5 Crore made up nearly 60% of regional launches as affordable stock shrank.

- Bengaluru

- Q1 2026 Average Price: ₹9,310 per sq ft

- Q2 2026 Average Price: ₹9,456 per sq ft

- Market Dynamics: Led YoY price appreciation indices, backed by a robust high-income tech sector and expanding Global Capability Centers (GCCs). Price momentum here outpaced many other zones, backed strictly by end-user buyer

- Pune

- Q1 2026 Average Price: ₹8,220 per sq ft

- Q2 2026 Average Price: ₹8,300 per sq ft

- Market Dynamics: Demonstrated outstanding mid-to-high-end stability, fueled by solid absorption from end-users in the manufacturing and IT sectors.

- Hyderabad

- Q1 2026 Average Price: ₹7,990 per sq ft

- Q2 2026 Average Price: ₹8,110 per sq ft

- Market Dynamics: Experienced a heavy 87% YoY surge in new launches early in the year before entering mid-year stabilization. Even with broader market normalization, Hyderabad proved its mettle through large township formats and rapid infrastructure growth in its tech corridors.

- Chennai

- Q1 2026 Average Price: ₹7,165 per sq ft

- Q2 2026 Average Price: ₹7,250 per sq ft

- Market Dynamics: Chennai avoided the high price volatility and speculative oversupply of other tier-1 cities, maintaining robust affordability with range-bound pricing and controlled new launches.

- Kolkata

- Q1 2026 Average Price: ₹6,290 per sq ft

- Q2 2026 Average Price: ₹6,380 per sq ft

- Market Dynamics: Stood as the most budget-friendly tier-1 market, retaining its position as a conservative market, with builders keeping a tight lid on supply to mirror the city’s measured absorption rates.

Key H1 Developments

- Q1 2026 (The Supply Leap): High developer confidence triggered a major release of over 126,000 fresh units in a single quarter. Sales for high-end homes jumped significantly, while affordable housing availability compressed due to rising input and land costs.

- Q2 2026 (Cyclical Moderation): The market experienced a planned mid-year pause, with sales volumes softening slightly in several regions. A combination of rising summer temperatures, seasonal dynamics, and cautious macroeconomic monitoring caused buyers to take more time closing deals, though capital values remained highly resilient.

Global Headwinds Impacting Builders

The Rising Cost of Building Materials (Global Conflict Impact)

On top of regular market changes, ongoing global wars and supply chain issues are pushing up the cost of building materials. Because crude oil prices have become volatile, it costs more to transport materials via diesel trucks. At the same time, the prices of essential building items—like steel, aluminum, copper, and petroleum-based PVC products—have seen sudden increases. Since these raw materials are essential for concrete structures, electrical work, and plumbing, builders are paying significantly more to finish their properties. To survive these rising costs, developers are raising prices on new launches and focusing even harder on completing existing buildings quickly before materials get any more expensive.

Shifted Timelines and Delayed Handovers

Because building materials cost more and are arriving late due to global trade blockages, developers are changing how they plan their construction timelines. Many builders are choosing to finish their current projects slowly and carefully rather than rushing into new ones. In some areas, buyers might see minor delays of a few months in getting their keys as developers take extra time to find affordable materials without cutting corners on quality. Turnkey builders are focusing completely on managing their funds tightly to keep their projects moving forward smoothly.

The Q3 2026 Outlook: What to Expect Next

As the residential market steps directly into Q3 2026, the temporary stagnation of the summer months is giving way to active preparation for the late-year festive buying window.

1. Finishing Current Projects First

Because builders launched a lot of new homes in the first half of the year, supply grew a bit faster than actual sales. In Q3, top-tier developers are focusing on building what they already started rather than buying new land on the edges of the cities. By focusing on finishing construction and handing over keys to buyers, they are keeping price growth steady and natural (around 5% to 8% a year) instead of letting prices spin out of control.

2. Early Launches for the Festive Season

The third quarter is when builders start introducing their best new properties right before the major holiday shopping season. Reputed developers are getting ready to open up new phases of premium homes. Buyers can look forward to more smart homes, high-tech features, self-contained mini-townships, and spacious, green luxury apartments in popular growing neighborhoods like the Dwarka Expressway in Delhi-NCR, Whitefield in Bengaluru, and the coastal areas of Chennai.

3. Better Home Loan Options

Because everyday costs and inflation are staying steady across the country, experts think the Reserve Bank of India might lower interest rates by the end of the quarter. If bank home loan rates drop, it will become cheaper to borrow money. This will be a huge help for buyers who have been waiting on the sidelines, giving them the perfect reason to finally buy a house right before the peak festive season begins.

The Takeaway: The structural framework that started with developer discipline in 2025 has matured beautifully. Heading deeper into the second half of 2026, the Indian housing sector remains highly resilient, fundamentally insulated from speculative risk, and anchored securely by long-term urban economic growth.

Verified.RealEstate: Transparency in Indian Property Deals

Verified.RealEstate is a trusted property platform in Tamil Nadu designed to bring complete transparency to the real estate market. The platform offers an all-in-one ecosystem of expert services and advanced tools (like its LandLens suite), covering every aspects for a residential market, from legal due diligence and land-use checks to building approvals and secure transactions to help users buy, sell, and manage property with confidence across Chennai.

Disclaimer: This article is for informational purposes only and does not constitute financial or real estate advice. All pricing and market data are indicative, compiled from reports by reputed industry institutions. Readers should conduct independent research and check RERA registrations before making any property investment.