Middle-class and lower-income families planning to purchase a home in urban India may be eligible for a home loan interest subsidy under the Pradhan Mantri Awas Yojana–Urban 2.0, commonly known as PMAY-U 2.0.

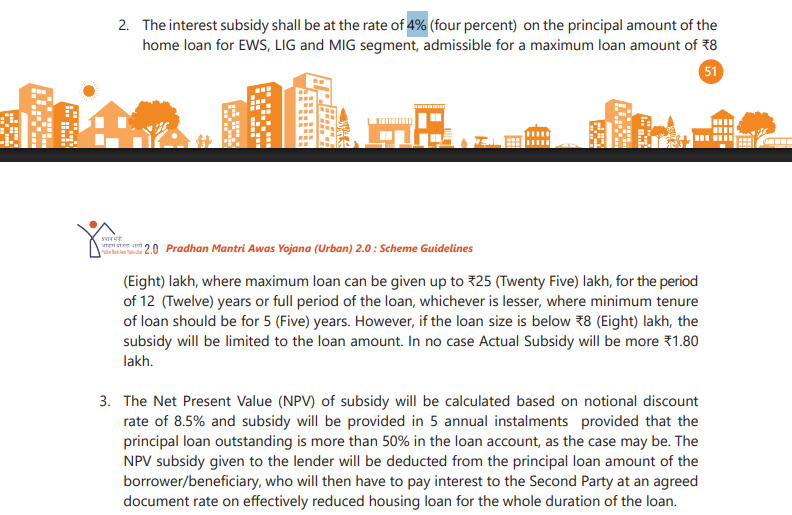

Under the Interest Subsidy Scheme component of PMAY-U 2.0, eligible families can receive a 4% interest subsidy on the first ₹8 lakh of a housing loan.

The maximum subsidy that can actually be released to a beneficiary is ₹1.80 lakh.

However, this should not be misunderstood as a 4% reduction on the borrower’s entire home loan. The subsidy applies only to the eligible portion of the loan and is subject to income, property-value and loan limits.

What Is the PMAY-U 2.0 Interest Subsidy Scheme?

PMAY-U 2.0 is a Central Government housing programme intended to help eligible urban families purchase, repurchase or construct a permanent house.

The Interest Subsidy Scheme is one of the components of the programme. It aims to make institutional housing finance more affordable for Economically Weaker Section, Low Income Group and Middle Income Group households.

The benefit is available for eligible home loans sanctioned and disbursed on or after September 1, 2024.

Is the Government Giving a 4% Home Loan?

No. The government is not offering a home loan at a flat interest rate of 4%.

The scheme provides a 4% interest subsidy on only the first ₹8 lakh of the home loan, calculated for an eligible tenure of up to 12 years.

For example, when a borrower takes a ₹20 lakh home loan, the subsidy will be calculated only on the eligible ₹8 lakh portion. The remaining ₹12 lakh will continue to carry the normal interest rate charged by the bank or housing finance company.

The total housing loan can be up to ₹25 lakh, but this does not mean the 4% subsidy applies to the full ₹25 lakh.

Maximum Home Loan Subsidy Available

The maximum interest subsidy released under the scheme is:

₹1.80 lakh per eligible beneficiary household

The scheme guidelines also mention a maximum net present value of ₹1.50 lakh. The actual subsidy released is distributed in five equal yearly instalments, subject to the loan continuing to meet the scheme conditions.

PMAY-U 2.0 Eligibility Criteria

A household must satisfy several conditions to qualify for the 4% home loan interest subsidy.

Household income

The household’s total annual income must not exceed ₹9 lakh.

The income groups covered are:

- Economically Weaker Section: annual household income up to ₹3 lakh

- Low Income Group: annual household income above ₹3 lakh and up to ₹6 lakh

- Middle Income Group: annual household income above ₹6 lakh and up to ₹9 lakh

The income limit applies to the combined household income and not merely the income of the primary loan applicant.

Maximum loan and property limits

- Loan amount: up to ₹25 lakh

- Property value: up to ₹35 lakh

- Carpet area: up to 120 sq. m (1,292 sq. ft)

- Loan tenure: more than 5 years

The 4% subsidy applies to the first ₹8 lakh for up to 12 years.

Eligibility Criteria

- Eligible:

- A family that does not own a permanent house anywhere in India and has not previously received housing assistance under specified Central Government housing schemes.

- A household where members taking a loan (jointly or separately) for the same property are considered as one unit for income and subsidy eligibility.

- Not Eligible:

- Families that already own a permanent house in India or have availed benefits under certain Central Government housing schemes.

- Properties for which the subsidy has already been claimed once; subsequent buyers cannot claim it again.

- Borrowers attempting to claim the subsidy after transferring their home loan to another lender, even if it was not claimed earlier.

How Will the Subsidy Be Paid?

The subsidy will not normally be paid directly to the borrower as unrestricted cash.

Eligible applicants must register their housing demand through the PMAY-U 2.0 unified web portal. After verification, the application is forwarded to the relevant participating lender.

The subsidy is released through the lending institution and credited to the borrower’s loan account.

It is provided in five equal yearly instalments, provided that:

- the home loan account remains active;

- the account is classified as standard;

- the borrower continues to meet the scheme conditions; and

- more than 50% of the original principal remains outstanding at the time of each subsidy release.

The subsidy amount is adjusted against the outstanding principal. The borrower then pays EMI based on the reduced loan balance and the lender’s applicable home loan rate.

Example of the 4% Home Loan Subsidy

Consider a family with an annual household income of ₹7 lakh purchasing a house worth ₹30 lakh.

The family takes a home loan of ₹22 lakh from a participating bank.

In this case:

- Annual household income: Within the ₹9 lakh limit

- Home loan: Within the ₹25 lakh limit

- Property value: Within the ₹35 lakh limit

- Eligible loan portion for subsidy: First ₹8 lakh

- Subsidy rate: 4%

- Maximum subsidy release: Up to ₹1.80 lakh

The remaining ₹14 lakh does not receive the 4% subsidy and continues under the lender’s normal home loan interest rate.

The exact benefit may differ depending on the loan tenure, outstanding principal, lender verification and continued compliance with the scheme conditions.

Can Existing Home Loan Borrowers Apply?

The Interest Subsidy Scheme covers eligible home loans sanctioned and disbursed on or after September 1, 2024.

Existing borrowers must check whether their loan date, income, house value and other conditions meet the PMAY-U 2.0 requirements. The lending bank or housing finance company must also participate in the scheme.

Borrowers should not assume that the subsidy will be applied automatically. Registration, lender verification and government approval are required.

What Homebuyers Must Understand

The PMAY-U 2.0 benefit is useful, but “4% home loan subsidy” can be misleading without context.

It applies only to eligible urban households, only on the first ₹8 lakh of the loan, and within set loan and property limits.

Homebuyers in Chennai can apply for PMAY benefits online through the official housing portal or offline through a participating bank or housing finance company. Applicants must submit Aadhaar details, income proof, property documents, bank information and a declaration confirming that the family does not own another permanent house. The lender then verifies the applicant’s eligibility and forwards the claim for subsidy approval.

Check eligibility on the official PMAY-U 2.0 portal or with your lender before proceeding.

Disclaimer: Scheme eligibility, subsidy approval and loan terms are subject to verification by the government, participating bank or housing finance company. Buyers should check the latest official guidelines before making a financial or property-purchase decision.