Imagine paying off a ₹1.86 crore home loan over 20 years, only to find out that the bank lost your original property title deeds. It is a homeowner’s worst nightmare.

The original Sale Deed is the legal backbone of your property. Without it, your title is compromised, selling the property becomes incredibly difficult, and securing a future loan or mortgage turns into a legal hurdle.

This exact nightmare became a reality for a Bengaluru homebuyer in the landmark case of Manoj Madhusudhanan vs. ICICI Bank Ltd. & Anr. (NCDRC, 2023). The ruling sent shockwaves through the banking sector, establishing a vital precedent for borrower rights.

If you are a home loan borrower, or plan to be one, here is everything you need to know about what happens if a bank misplaces your papers, your legal rights to compensation, and how to protect your investment.

The Landmark Case: Manoj Madhusudhanan vs. ICICI Bank Ltd.

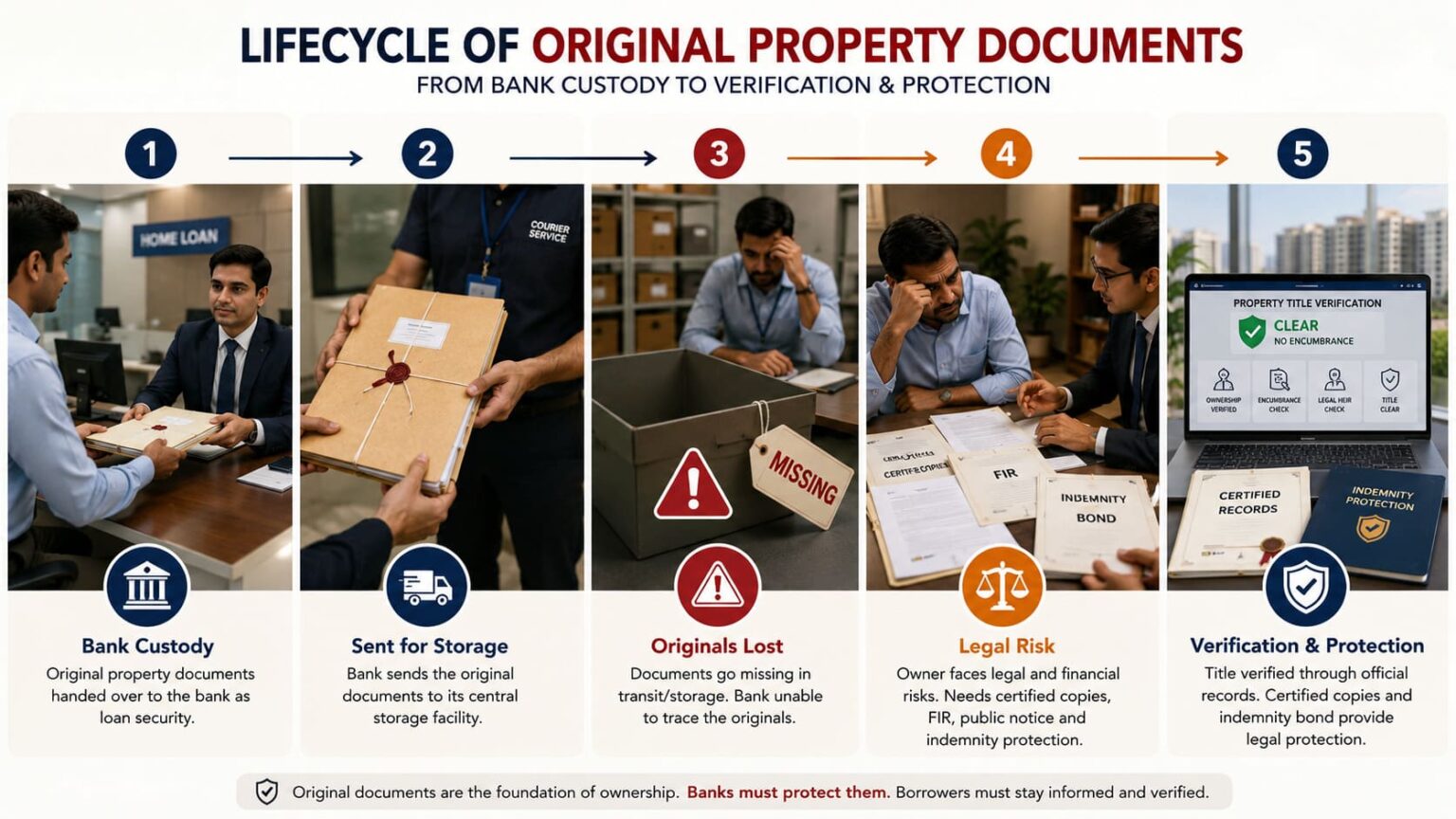

In April 2016, Manoj Madhusudhanan took a housing loan of ₹1.86 crore from ICICI Bank to purchase a prime site in Rajarajeshwari Nagar, Bengaluru. Following standard banking procedures, the original property documents were handed over to the bank as security for the loan.

The nightmare began when the borrower requested copies of the registered deeds.

How 10 kg of Legal Papers Disappeared into Thin Air

ICICI Bank revealed that it had dispatched the original title documents from Bengaluru to its central storage facility in Hyderabad via Blue Dart Express Ltd.

When the courier consignment arrived at the storage facility, the contents relating to Manoj’s property were completely missing. Curiously, the bank noted that the transit package weighed only 7 kg instead of its original 10 kg dispatch weight. Blue Dart later issued a formal apology, admitting the documents were lost in transit, and filed an FIR with the Cyberabad Police.

The Double Standard in Compensation

When dealing with the borrower, ICICI Bank allegedly offered a meager settlement equivalent to just two monthly EMIs. However, the bank concurrently sent a legal notice to Blue Dart, demanding a massive ₹2.5 crore in compensation for the loss.

This stark discrepancy became a focal point in the subsequent legal battle, proving that the bank internally viewed the loss as a severe financial hit while downplaying it to the consumer.

Banking Ombudsman Stage

Before approaching the NCDRC, Manoj Madhusudhanan first went to the Banking Ombudsman on 14 August 2016. On 22 September 2016, the Banking Ombudsman directed ICICI Bank to:

give duplicate copies of the lost documents,

publish a public notice regarding the loss,

pay ₹25,000 as compensation for deficiency in service.

But the borrower was not satisfied. He argued that the public notice was published only in Bengaluru, while the documents were lost in Hyderabad. He also argued that duplicate or certified copies cannot fully replace the legal value of original title documents.

What the Consumer Forum (NCDRC) Ruled

Dissatisfied with a minor intervention by the Banking Ombudsman, the borrower dragged ICICI Bank to the National Consumer Disputes Redressal Commission (NCDRC) in New Delhi. He claimed tracing of the original documents and ₹5 crore compensation for mental agony, loss and deficiency in service. His main argument was that the loss of original title documents weakened his title position, affected the market value of the property

Key Legal Principal Established by NCDRC:

A bank cannot outsource its liability. When a borrower deposits original title deeds as security, the bank acts as a bailee and carries an absolute duty of care. Any internal arrangements with couriers or third-party storage vendors are strictly the bank's internal business—not the borrower’s problem.

The NCDRC explicitly observed that the loss of original ownership papers drastically compromises a homeowner’s legal title and market resale value.

The NCDRC Order & Financial Penalties:

The ₹5 Crore Claim Was Not Fully Accepted

The NCDRC did not accept the full ₹5 crore claim. It noted that the property was mortgaged for around ₹1.95 crore on 22 April 2016, and that the ₹5 crore valuation seemed inflated considering the short duration between the mortgage and the filing of the complaint.

But the Commission also said that the issue was not about fixing the property’s full market value. The real issue was compensation for deficiency in service and protection against future loss.

The Commission partly allowed the complaint, directing ICICI Bank to:

- Obtain and reconstruct certified copies of all lost original documents at its own cost.

- Execute a legally binding Indemnity Bond in favor of the borrower to cover future risks.

- Pay ₹25 Lakhs as compensation to the borrower for severe deficiency in service and mental agony.

- Pay ₹50,000 as litigation costs.

Current Legal Status (Supreme Court Appeal)

It is crucial for property owners to note that ICICI Bank challenged this NCDRC order before the Supreme Court of India (Civil Appeal Nos. 8132–8133 of 2023). In December 2023, the Supreme Court issued a notice and stayed the operative portion of the NCDRC order (including the payout). As per recent judicial reports, the matter remains pending in the Supreme Court for final adjudication.

Why Certified Copies Don’t Fully Solve the Problem

When a bank offers to “just get you certified duplicates from the Sub-Registrar,” they are masking a permanent financial risk. Here is why losing the originals damages your asset:

- The Re-sale Red Flag: Future buyers and property lawyers look at certified copies with immediate suspicion. It triggers fears of ownership disputes or fraudulent double-mortgages.

- Loan Refusal: If you ever try to transfer your loan to another bank (balance transfer) or take a top-up loan, secondary lenders will routinely reject properties missing original deeds.

- The Equitable Mortgage Trap: In India, an “equitable mortgage” is created simply by delivering original title deeds to a lender. If the originals are out in the wild, there is a lingering risk they could be misused by third parties to raise unauthorized funds.

An indemnity bond is a legal safety promise from the bank that protects the borrower from such future losses caused by the bank losing the original property documents.The RBI Steps In: Strict Rules & Daily Penalties

To completely eliminate this systemic banking negligence, the Reserve Bank of India (RBI) implemented a stringent regulatory framework that protects borrowers.

If a bank loses or delays the return of your original documents, the RBI guidelines outline a clear mandate:

| Timeline / Event | Bank’s Mandatory Action |

| Loan Closure Deadline | Bank must return all original property documents within 30 days of full loan repayment. |

| If Documents are Lost | Bank must actively assist the borrower in obtaining certified/reconstructed copies from authorities at the bank’s own expense. |

| The 30-Day Grace Window | The bank gets an additional 30 days to sort out the copies (Total 60 days from loan closure). |

| Daily Financial Penalty | If the delay extends beyond 60 days, the bank MUST pay the borrower ₹5,000 per day for every single day of delay. |

Action Plan: What to Do If Your Bank Loses Your Deeds

If you discover your bank or non-banking financial company (NBFC) has misplaced your original property file, immediately execute these four steps:

1.Demand Written Acknowledgment:Immediate.

Do not rely on verbal assurances from branch managers. Force the bank to issue a formal letter or email admitting they are unable to locate your original property documents.

2.Ensure an FIR is Filed:Within 7 Days.

Verify that a police complaint (First Information Report) has been filed specifically detailing the lost documents, tracking numbers, and the property details. Obtain a certified copy of the FIR.

3.Mandate a Public Notice:Within 15 Days.

Ensure the bank publishes a clear “Loss of Documents” public notice in at least two prominent newspapers (one English daily and one local regional language newspaper) covering both the city where the property is located and the city where the documents went missing.

4.File an RBI Ombudsman/Consumer Complaint:Post 30 Days.

If the bank fails to deliver reconstructed copies and a registered Indemnity Bond within 30 days of loan closure, escalate the matter directly to the RBI Banking Ombudsman and file a consumer case demanding the ₹5,000 daily penalty along with mental agony compensation.

Buyer’s Beware: What if a Seller Has No Originals?

If you are looking to purchase a resale property and the seller claims, “The originals were lost, but I have certified copies and the bank’s closure letter,” proceed with extreme caution.

It does not mean you should abandon the deal, but you must complete strict enhanced due diligence:

- Check the original police index records to ensure the FIR is genuine.

- Verify the public notice clippings in newspaper archives.

- Obtain a fresh Encumbrance Certificate (EC) for the last 13 to 30 years to check for hidden liabilities.

- Insist that the seller signs an absolute Indemnity Bond indemnifying you against any future claims arising out of the missing original documents.

Your property title is your financial security. Don’t let corporate or banking negligence dilute your hard-earned ownership.